Inside the Race to Build the World's First Commercial Solid-State Battery in 2026

If there is a single technology that could transform everything from electric vehicles to grid-scale energy storage to consumer electronics in one stroke, it is the solid-state battery. After decades of laboratory promise and false starts, the race to commercialize this revolutionary technology has entered its most intense phase, with major automakers, battery manufacturers, and startups investing billions in pursuit of the holy grail of energy storage.

Why Solid-State Batteries Matter: The Promise and the Challenge

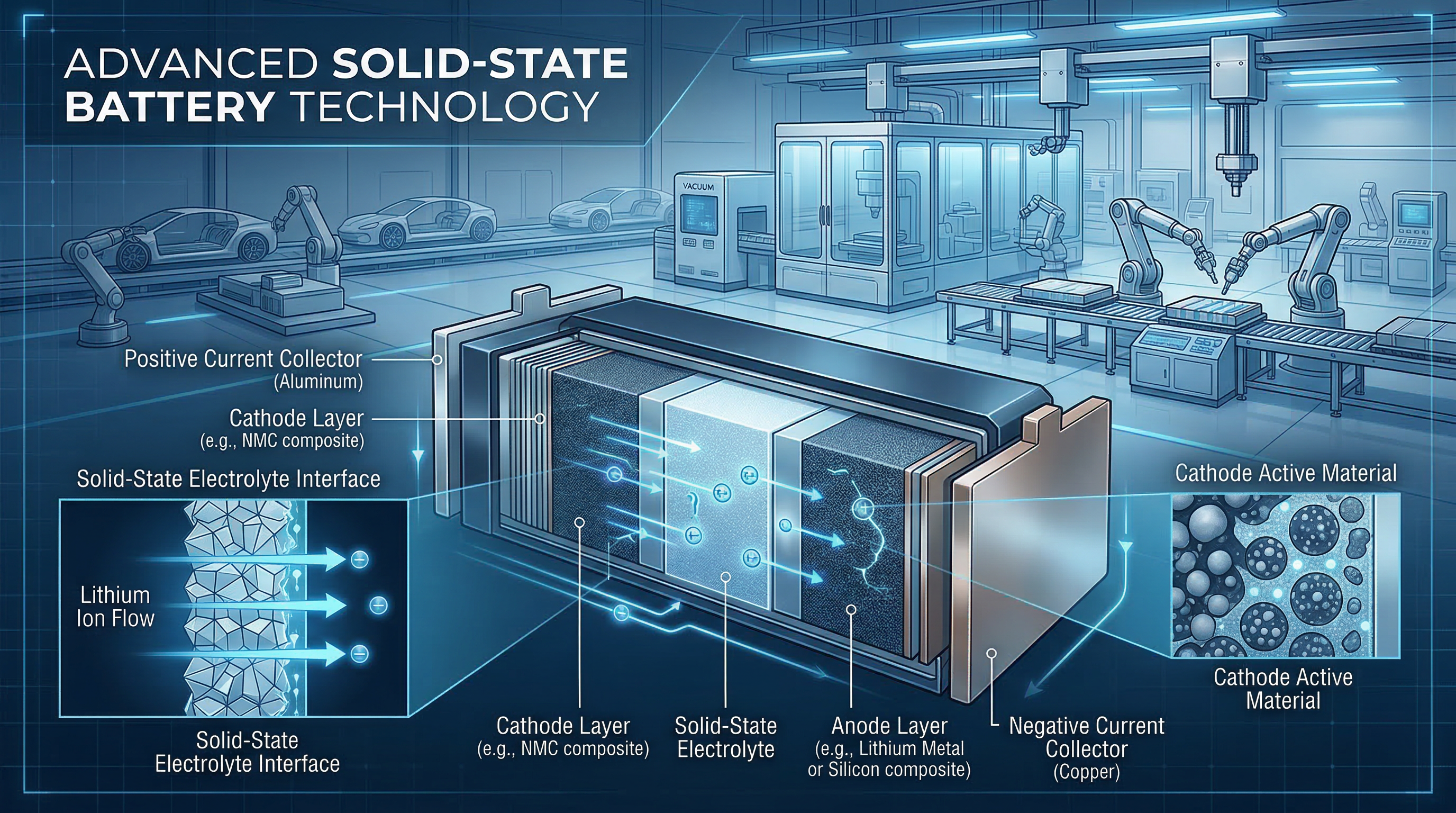

The concept behind solid-state batteries is elegantly simple yet profoundly transformative. Conventional lithium-ion batteries use a liquid electrolyte as the medium through which lithium ions shuttle between the anode and cathode during charging and discharging cycles. This liquid electrolyte works well enough, powering everything from smartphones to electric vehicles to grid storage systems. But it comes with significant limitations that constrain battery performance and safety.

Solid-state batteries replace the liquid electrolyte with a solid material, typically a ceramic, glass, or polymer. This single change unlocks a cascade of benefits that address nearly every major limitation of current battery technology. The solid electrolyte is non-flammable, eliminating the fire risk that has plagued lithium-ion batteries. It enables the use of lithium metal anodes, which offer dramatically higher energy density than the graphite anodes used in conventional batteries. It allows for faster ion transport, enabling rapid charging. And it is more stable over many charge cycles, promising longer battery lifespans.

Industry analysts project that solid-state batteries could enable electric vehicles with ranges exceeding 600 miles on a single charge, charging times under 15 minutes, and battery lifespans measured in decades rather than years. These improvements would eliminate the primary barriers to mass EV adoption including range anxiety, charging inconvenience, and concerns about battery replacement costs.

The Key Players: Who Is Leading the Race

The competition to commercialize solid-state batteries spans continents and involves some of the largest corporations in the automotive and electronics industries, as well as ambitious startups. Each player brings different technological approaches, timelines, and resources to the challenge.

Toyota: The Patent Leader with Long-Term Vision

Toyota has been working on solid-state battery technology for more than a decade and holds one of the largest patent portfolios in the field, with over 1,000 patents related to solid-state battery technology. The Japanese automaker has publicly announced plans to introduce solid-state batteries in hybrid vehicles in the mid-2020s, with all-electric applications to follow.

According to public statements from Toyota executives, the company is targeting batteries that deliver over 1,000 kilometers (approximately 620 miles) of range and can charge in 10 minutes or less. Perhaps most ambitiously, Toyota has stated that its solid-state batteries are designed for a lifespan of 40 years or more, which would fundamentally change the economics of electric vehicle ownership.

Toyota's approach focuses on sulfide-based solid electrolytes, which offer high ionic conductivity but present manufacturing challenges. The company has built pilot production lines and is working to scale up manufacturing processes while addressing durability and cost challenges. Industry observers note that Toyota's timeline has shifted multiple times, reflecting the technical difficulties inherent in moving from laboratory prototypes to mass production.

Samsung SDI: Electronics Giant Pivots to Automotive

Samsung SDI, the battery division of the Korean electronics conglomerate, has emerged as another major player in solid-state battery development. The company has demonstrated prototype batteries using oxide-based solid electrolytes and has announced ambitious performance targets including ranges exceeding 600 miles and charging times competitive with conventional refueling.

Samsung's oxide electrolyte approach offers different tradeoffs compared to sulfide electrolytes. Oxide electrolytes are generally more stable in air and offer better safety characteristics, but they can be more difficult to process and may have lower ionic conductivity. Samsung has invested heavily in developing manufacturing techniques to address these challenges, building on its decades of experience in battery production for consumer electronics.

The company has stated plans to begin pilot production of solid-state batteries in the mid-2020s, with mass production targeted for the late 2020s. Samsung has secured supply agreements with several automotive manufacturers, positioning itself to supply batteries for multiple EV platforms when the technology reaches commercial readiness.

QuantumScape: The Silicon Valley Bet on Ceramic Separators

QuantumScape represents a different approach to the solid-state battery challenge. The Silicon Valley startup, backed by Volkswagen and other major investors, focuses specifically on a proprietary ceramic separator technology that addresses one of the fundamental challenges in solid-state batteries: dendrite formation.

Dendrites are needle-like structures of lithium metal that can grow through the solid electrolyte during charging cycles, eventually causing short circuits and battery failure. QuantumScape claims its ceramic separator technology prevents dendrite penetration while maintaining high ionic conductivity and flexibility. The company has demonstrated single-layer cells with promising performance characteristics and is working to scale up to multi-layer cells suitable for automotive applications.

QuantumScape went public via SPAC in 2020, raising significant capital to fund its development and manufacturing scale-up. The company has faced both enthusiasm and skepticism from investors and industry observers, with its stock price reflecting the high-risk, high-reward nature of breakthrough battery technology. QuantumScape has partnerships with Volkswagen for eventual vehicle integration and is building pilot manufacturing capacity to demonstrate production scalability.

Chinese Manufacturers: CATL, BYD, and the Pragmatic Approach

Chinese battery manufacturers CATL and BYD, already the world's largest producers of lithium-ion batteries, are pursuing solid-state technology along with multiple other next-generation battery chemistries. Their approach tends to be more pragmatic and incremental, focusing on semi-solid and hybrid designs that incorporate some solid-state elements while maintaining compatibility with existing manufacturing infrastructure.

CATL has announced research into solid-state batteries and has demonstrated prototype cells, but the company appears to be hedging its bets by also investing heavily in advanced lithium-ion chemistries, sodium-ion batteries, and other technologies. This diversified strategy reflects the uncertainty about which technology will prove most practical for mass production and the need to continue improving current technology while developing future alternatives.

BYD similarly pursues multiple battery technology pathways in parallel. The company has made significant announcements about both solid-state battery research and improvements to conventional battery technologies. Industry analysts suggest that Chinese manufacturers may wait to see which technical approaches prove most viable before committing fully to large-scale solid-state production.

Solid-State Battery Development Timeline

Expected commercialization timelines from major manufacturers (based on public announcements)

The Technical Hurdles: Why Commercialization Is So Difficult

If solid-state batteries offer such compelling advantages, why are they not already in mass production? The answer lies in a series of interconnected technical and manufacturing challenges that have proven extraordinarily difficult to solve at scale.

Dendrite Formation and Interface Stability

When lithium metal anodes are used in solid-state batteries, there is a risk of dendrite formation, where metallic lithium grows in needle-like structures that can penetrate the solid electrolyte. Once a dendrite bridges the gap between anode and cathode, it creates a short circuit that renders the battery unusable and potentially dangerous.

Different solid electrolyte materials have varying resistance to dendrite penetration. Ceramic electrolytes generally offer good dendrite resistance but are brittle and can crack under mechanical stress or thermal cycling. Polymer electrolytes are more flexible but typically have lower ionic conductivity and may be more susceptible to dendrite growth. Finding the right balance of properties has proven extremely challenging.

The interface between the solid electrolyte and the electrode materials is another critical challenge. In liquid electrolyte batteries, the liquid naturally maintains intimate contact with electrode surfaces as the battery expands and contracts during charging. With solid materials, maintaining good interfacial contact is much more difficult. Poor contact leads to high resistance, reduced performance, and accelerated degradation.

Manufacturing Scale and Cost

Even when solid-state batteries demonstrate excellent performance in the laboratory, scaling up production introduces entirely new challenges. Solid electrolytes must be extremely thin to minimize resistance while being completely uniform and defect-free. A single pinhole or crack can lead to catastrophic failure.

Current lithium-ion battery manufacturing relies on well-established processes including electrode coating, calendaring, cell assembly, and formation. Solid-state batteries require fundamentally different manufacturing approaches. Ceramic electrolytes may need to be sintered at high temperatures. Maintaining alignment and contact across multiple layers is more difficult with solid materials. Quality control requirements are more stringent because defects that would merely reduce performance in conventional batteries can cause complete failure in solid-state cells.

The cost implications are significant. Industry estimates suggest that early solid-state batteries may cost two to three times as much as conventional lithium-ion batteries to produce. Only with substantial production volume and process optimization will costs decline to competitive levels. This creates a chicken-and-egg problem: manufacturers need volume to drive down costs, but high costs limit adoption and volume.

Temperature Sensitivity and Operating Range

Many solid electrolyte materials exhibit temperature-dependent ionic conductivity, meaning they perform well at elevated temperatures but poorly in cold conditions. This creates challenges for automotive applications where batteries must operate reliably across a wide temperature range, from hot desert summers to cold winter conditions.

Some solid electrolyte materials require heating to achieve acceptable performance, which adds system complexity and energy consumption. Others become brittle at low temperatures, risking mechanical failure. Developing solid electrolytes that maintain good performance across the full automotive temperature range remains an active area of research.

Solid-State vs Conventional Li-ion: Key Differences

Related Technology: While solid-state batteries promise revolutionary improvements, sodium-ion batteries offer a more immediately available alternative for many applications. Learn about this emerging technology in our comprehensive guide: The Future of Green Technology in 2026.

Alternative Approaches: Semi-Solid and Hybrid Designs

Recognizing the challenges of all-solid-state batteries, some manufacturers are pursuing intermediate approaches that capture some benefits while avoiding the most difficult technical hurdles.

Semi-Solid Batteries

Semi-solid batteries use a combination of solid and liquid or gel electrolytes. These designs may use solid electrolyte separators combined with liquid or gel electrolytes in the electrode regions, or they may use solid electrolytes with small amounts of liquid to improve interfacial contact. While not achieving the full benefits of all-solid-state designs, these hybrid approaches can offer significant improvements over conventional batteries while being easier to manufacture with existing production equipment.

Solid-State for Specific Applications

Some companies are targeting solid-state batteries for specific niche applications where the technology's advantages justify higher costs. Medical devices, aerospace applications, and premium consumer electronics may adopt solid-state batteries before mass-market automotive applications. These early deployments would allow manufacturers to refine their technology and build production experience before attempting the massive scale required for electric vehicles.

The Sodium-Ion Alternative: A Parallel Revolution

While solid-state lithium batteries pursue the performance frontier, sodium-ion batteries are emerging as a compelling alternative focused on cost and resource availability. Sodium is roughly 1,000 times more abundant than lithium and can be extracted from seawater, eliminating supply chain concerns that constrain lithium-based technologies.

Sodium-ion batteries use similar cell designs to lithium-ion batteries but substitute sodium for lithium in the electrolyte and electrode materials. They typically offer lower energy density than lithium batteries, making them less suitable for long-range electric vehicles. However, for stationary energy storage, short-range urban vehicles, and backup power applications, sodium-ion batteries may offer better economics.

Major manufacturers including CATL and BYD have announced sodium-ion battery products and are building production capacity. These batteries are expected to reach commercial markets in the mid-2020s, potentially before solid-state lithium batteries achieve mass production. The coexistence of multiple battery technologies, each optimized for different applications, appears increasingly likely.

Deep Dive: To understand how solid-state batteries fit into the broader landscape of green technology innovations, read our pillar article: The Future of Green Technology in 2026: Complete Guide to Next-Gen Batteries, EV Infrastructure, and Electric Aviation.

Manufacturing Breakthroughs and Production Scaling

Recent developments suggest that some of the manufacturing challenges may be yielding to engineering solutions. Several companies have announced progress in key areas that could enable commercial production.

Thin-Film Deposition Techniques

Advanced thin-film deposition methods, adapted from semiconductor manufacturing, are being applied to solid electrolyte production. These techniques can create very thin, uniform electrolyte layers with precise thickness control. While slower and more expensive than conventional battery coating processes, they may enable the production of high-performance cells for premium applications.

Roll-to-Roll Manufacturing

Some developers are working on adapting existing roll-to-roll manufacturing processes used for conventional batteries to solid-state production. If successful, these approaches could leverage existing manufacturing infrastructure and expertise, reducing capital requirements and accelerating commercialization. However, maintaining the necessary precision and quality control in continuous manufacturing remains challenging.

Artificial Intelligence in Material Discovery

AI and machine learning are accelerating the discovery and optimization of solid electrolyte materials. Computational models can screen millions of potential material compositions to identify promising candidates for experimental validation. This approach has already led to the discovery of several new solid electrolyte materials with improved properties, and it continues to expand the toolkit available to battery developers.

AI in Battery Development: Artificial intelligence is playing an increasingly important role in battery research. Learn more in our article: How AI Is Revolutionizing the Climate Fight in 2026.

Early Research Phase

Academic and industrial laboratories demonstrate solid-state battery prototypes with promising performance in controlled conditions. Toyota begins major research program.

Technology Validation

QuantumScape founded with VW backing. Multiple companies announce solid-state development programs. First large-scale pilot manufacturing lines built.

Scaling Challenges

Companies encounter manufacturing difficulties. Timelines extended as technical hurdles prove harder than expected. Some startups struggle with commercialization.

Commercial Introduction

First commercial solid-state batteries expected in premium vehicles and niche applications. Mass market adoption remains years away as production scales up.

Market Impact and Industry Implications

The successful commercialization of solid-state batteries would have profound implications across multiple industries and could accelerate the global transition to electric transportation and renewable energy.

Electric Vehicle Revolution

Solid-state batteries could eliminate the primary objections to EV adoption. Range parity or superiority compared to gasoline vehicles would make electric cars suitable for all driving needs, not just local commuting. Fast charging comparable to refueling times would eliminate charging anxiety. Long battery lifespans exceeding vehicle lifespans would reduce total cost of ownership below comparable gasoline vehicles.

The EV market could shift from primarily serving early adopters and environmentally motivated buyers to capturing mainstream mass market consumers. Industry analysts project that solid-state batteries could accelerate EV market penetration by five to ten years compared to trajectories based on incremental improvements to conventional battery technology.

Grid-Scale Storage Economics

While automotive applications receive the most attention, solid-state batteries could also transform grid-scale energy storage. The higher energy density would reduce the physical footprint and land requirements for storage installations. The improved safety would simplify siting and permitting. The longer lifespans would improve project economics by extending the period over which initial capital investments are amortized.

These improvements could make renewable energy plus storage competitive with fossil fuel generation in more markets and enable higher renewable penetration on the grid. The energy transition could accelerate significantly if storage costs decline and performance improves.

Supply Chain and Geopolitics

Solid-state batteries could reshape global supply chains and the geopolitics of energy storage. Countries and companies that lead in solid-state technology may gain strategic advantages similar to current leadership in semiconductor manufacturing. The potential to reduce dependence on specific battery raw materials like cobalt could ease supply chain vulnerabilities and ethical concerns about mining practices.

However, solid-state batteries will create demand for new materials including specialized ceramics and solid electrolyte components. New supply chains will need to be established, potentially creating new dependencies and competitive dynamics.

Investment Landscape and Corporate Strategy

The race to commercialize solid-state batteries has attracted billions in investment from automotive companies, battery manufacturers, venture capitalists, and governments. Major automakers including Volkswagen, Toyota, Ford, BMW, Hyundai, and others have invested in solid-state development either through internal R&D or partnerships with battery developers.

Battery manufacturers face strategic decisions about how much to invest in solid-state technology while continuing to improve and produce conventional batteries that generate current revenue. The risk of investing too heavily in a technology that may not reach commercialization must be balanced against the risk of falling behind competitors if solid-state batteries succeed.

Startups like QuantumScape have raised substantial capital but face the challenge of delivering commercial products before funding runs out. The capital intensity of battery manufacturing means that even promising technology can fail if commercialization takes longer than expected and cash runs short.

The Road Ahead: Realistic Timelines and Expectations

Despite the promise of solid-state batteries and the intensity of development efforts, realistic assessment suggests that widespread commercial deployment remains several years away. Most industry observers expect limited introduction of solid-state batteries in premium vehicles or niche applications in the late 2020s, with mass market adoption unlikely before the 2030s.

The path from laboratory prototype to mass production has proven longer and more difficult than initial optimistic projections suggested. Technical challenges including dendrite formation, interface stability, manufacturing scale-up, and cost reduction remain substantial. Multiple companies have delayed their initially announced timelines as they encountered these difficulties.

However, progress continues. The number of players, the scale of investment, and the strategic importance of success suggest that solid-state batteries will eventually reach commercialization. The question is not if but when, and whether they will arrive soon enough to have major impact on climate goals that require rapid transportation electrification in the coming decade.

Conclusion: The Battery Revolution Continues

The race to build commercial solid-state batteries represents one of the most significant technology competitions of the decade. Success would accelerate the electric vehicle revolution, enable higher renewable energy penetration, and contribute substantially to climate change mitigation. The companies and countries that master this technology may gain strategic advantages lasting decades.

Yet even as the solid-state battery race continues, conventional lithium-ion batteries continue to improve, becoming cheaper, more energy-dense, and longer-lasting each year. Sodium-ion batteries are emerging as an alternative for cost-sensitive applications. The future of energy storage will likely include multiple technologies, each optimized for specific applications rather than a single dominant solution.

For consumers and investors, the solid-state battery story is one to watch closely but with realistic expectations. The revolutionary improvements promised by this technology are real and achievable, but the timeline for mass market impact remains uncertain. In the meantime, incremental improvements to existing battery technology continue to drive EV adoption and renewable energy deployment, bringing us closer to a sustainable energy future even as we await the next battery revolution.

Continue Exploring: Solid-state batteries are just one piece of the green technology puzzle. For a comprehensive overview of all the technologies transforming sustainable energy in 2026, read our complete guide: The Future of Green Technology in 2026.

About the Authors

Future Green Tech Editorial Team consists of climate technology journalists, engineers, and analysts who track the latest developments in green technology from research labs to commercial deployment. Our team combines technical expertise with investigative journalism to provide readers with accurate, in-depth analysis of sustainable technologies shaping our future. All articles are fact-checked and based on publicly available data, peer-reviewed research, and official company announcements.